Diversification is one of the most widely accepted principles in finance. It appears in textbooks, professional frameworks, and institutional portfolios across the world. And yet, for many investors, diversification feels deeply unsatisfying in practice.

A diversified portfolio rarely looks optimal in the moment. It almost always contains something that seems unnecessary, outdated, or plainly wrong. During strong equity markets, defensive assets feel like dead weight. During inflationary periods, bonds feel fragile. During calm environments, insurance-like assets feel redundant.

At any given time, it can feel as though a simpler, more concentrated portfolio would have been the rational choice. You have probably heard “Stocks for the long-run“, right, so why bother with diversifiers?

The principals at Resolve Asset Management often paraphrase a very strong quote which resonates with this idea:

“If you don’t at all times hate at least one asset in your portfolio, you are not diversified enough.”

This tension is not accidental. Diversification was never designed to feel good in the short term. It was designed to work across full market cycles, including environments that are uncomfortable, surprising, or difficult to predict in advance.

Understanding diversification therefore requires more than understanding statistics or correlations. It requires understanding how human psychology interacts with uncertainty, how markets rotate leadership over time, and what diversification is actually meant to achieve. This article explores why diversification so often feels wrong before it works—and why that discomfort is often the very reason it works at all.

ASSET CLASS RETURNS

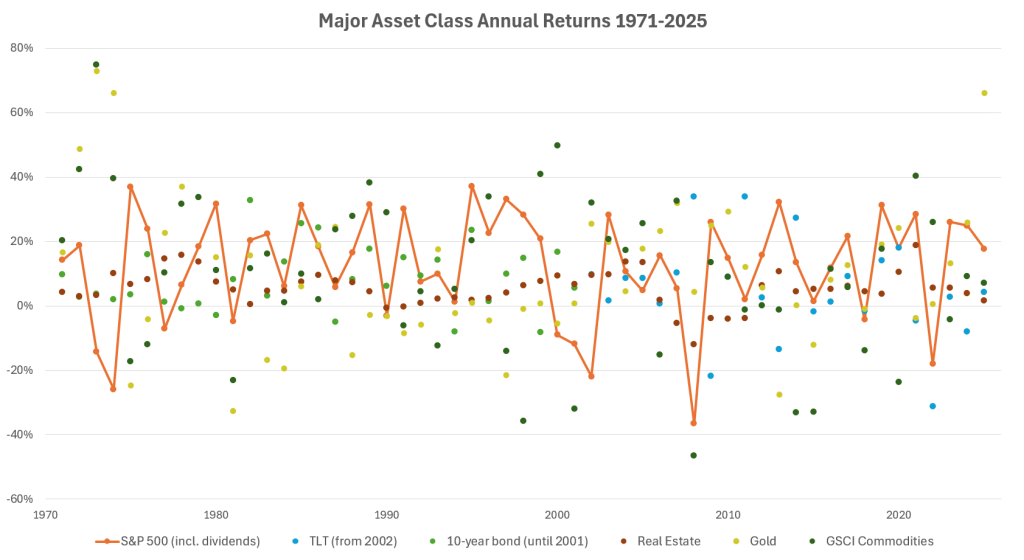

Before we jump into discussing the discomforts of diversification, I will leave you with the below chart. This depicts the annual returns of major asset classes over the period 1971-2025. Considering that most investors tend to focus on stocks, the S&P 500 (including dividends) has been highlighted as the orange line, and other asset class returns depicted with dots. We will return to this chart further down in this article, with a bit more added All-Weather style flavour.

Looking at the S&P 500 line, there is quite a lot of variance from one year to the next: from nearly -40% to +40%, and everything in between.

One interesting note is that while the expected returns for the stock market is said to be around 7-10% p.a., it only happened twice during this period that stock market returns were in that range: in 1992 and 1993.

All other asset classes are spread rather evenly across the range. But there are three problems that cause discomfort for most investors.

Firstly, during the years when the stock market is one of the best performing assets, you don’t want to dilute your returns.

Secondly, the best performing diversifier is rarely the same every year, but it could be bonds, it could be gold, or it could be commodities. How can you make sure to always pick the “correct” diversifier?

Thirdly, stocks have faced several deep declines (also intra-year drawdowns that are not fully visible here), which will give you a headache if you elect to ignore diversification.

WHY OUR BRAINS DISLIKE DIVERSIFICATION

Human decision-making evolved in environments very different from modern financial markets. As a result, many of our intuitive responses to uncertainty are poorly suited to long-term investing. Diversification, in particular, runs directly against several deeply ingrained cognitive tendencies.

Recency Bias

Recency bias is the tendency to overweight recent experiences when forming expectations about the future. If an asset has performed well over the past few years, it feels natural to assume that it will continue to do so. Conversely, assets that have lagged feel structurally flawed or obsolete. The financial markets are in a “new normal” state.

Diversified portfolios deliberately resist this instinct. They maintain exposure to assets that may have underperformed recently precisely because markets tend to move in cycles. What has worked lately is often already priced in, while what has disappointed may be positioned for recovery when conditions change.

Psychologically, this is difficult. Holding an asset that has not delivered visible rewards for years can feel like ignoring obvious information. In reality, it is often an attempt to avoid extrapolating the recent past too far into the future. Most often, it is also difficult to correctly predict when the tides turn.

Performance Chasing

Closely related to recency bias is performance chasing: the impulse to allocate more capital to what has already done well. Performance chasing is reinforced by financial media, peer conversations, and even professional incentives. Success stories are visible and compelling; slow, steady resilience is not.

Diversification requires the opposite behavior. It requires maintaining balance rather than concentrating on recent winners. It often requires trimming assets that have outperformed and adding to those that have lagged—a process that can feel counterintuitive and emotionally uncomfortable.

From a psychological standpoint, it can feel like selling strength and buying weakness. From a portfolio-construction standpoint, it is a way of systematically managing risk and avoiding overexposure to any single outcome.

Performance chasing is closely related to trend following, which is a completely viable investment strategy. However, trend-followers closely monitor positions for exit triggers, not to get caught when the cycles turn.

Social Comparison and Regret

Investing does not happen in isolation. Investors are constantly exposed to the choices and outcomes of others. Opportunity cost sits in this bucket. When a single asset or strategy dominates headlines, diversified investors may experience a sense of regret or inadequacy. The question “Why didn’t I just own that?” can become persistent and distracting.

Diversification tends to produce fewer moments of extreme relative outperformance. Its benefits are subtle and cumulative rather than dramatic. This makes it psychologically challenging in environments where success is often framed in terms of beating benchmarks or peers over short periods.

The emotional discomfort of underperforming popular strategies, even temporarily, can lead investors to abandon diversification precisely when it is most needed.

When emotion takes over, we should try to focus on the correlation matrix, not each sleeve’s absolut return.

WHY THERE IS ALWAYS A “LOSER” IN A DIVERSIFIED PORTFOLIO

A diversified portfolio is not designed to have all components performing well at the same time. In fact, if every asset were rising together, diversification would offer little protection, as they would then also fall together. Its effectiveness depends on differences (sometimes sharp differences) in how assets respond to changing conditions.

As a result, there is almost always a visible “loser” in a diversified portfolio. This might feel annoying, but is a feature (not a bug).

At times, equities dominate returns and defensive assets appear unnecessary, boring, and just a drag. At other times, interest-rate sensitive assets struggle while inflation-linked assets provide protection. There are periods when real assets shine and periods when they stagnate. Leadership rotates, often unpredictably and sometimes abruptly.

This rotation is not a flaw. It is the mechanism by which diversification works.

When one asset class is under pressure, another may be benefiting from the same conditions. Economic growth, inflation, monetary policy, and risk sentiment do not move in straight lines. They evolve, interact, and occasionally reverse in ways that are difficult to forecast with confidence. It doesn’t even need to be absolute numbers of these factors, but the market’s expectation of future developments that abruptly change: what the business climate, inflation or interest rate is expected to be in 12 months time, for example.

A diversified portfolio accepts this uncertainty. Rather than trying to predict which economic environment or asset will lead next, it holds a range of assets that respond differently to different environments. The visible underperformance of one component is often the cost of maintaining exposure to another that may become essential later.

Importantly, the presence of a “loser” does not mean the portfolio is broken. It often means it is doing exactly what it was designed to do: maintaining balance in a world where conditions are constantly changing.

As it is a feature rather than a bug, we can also take advantage of it when we rebalance the portfolio. This is exactly when the rebalancing premium is earned: when selling relative winners to buy relative losers, and over time earn more money than the average return of the owned assets.

WHAT DIVERSIFICATION IS ACTUALLY DESIGNED TO DO

Many frustrations with diversification stem from misunderstandings about its purpose. Diversification is often evaluated using the wrong criteria. The investor needs to re-evaluate or remind themselves of their outlook on diversification, and consider why it is used.

Not Maximizing Short-Term Returns

Diversification is not designed to maximize returns over short horizons. Concentration almost always wins that contest—until it doesn’t. A highly concentrated portfolio can outperform dramatically when conditions are favorable, but it also carries a higher risk of severe drawdowns when conditions change.

Diversification intentionally sacrifices some upside in strong environments in exchange for greater resilience across a wider range of outcomes. This trade-off is rational for investors whose primary goal is long-term capital preservation and compounding rather than short-term optimization.

This concept was clearly illustrated in a memo titled “Fewer Losers, or More Winners?” by Howard Marks, wherein he describes a pension fund manager who, over a 14-year period, was never in the top 27th percentile of the pension fund universe in annual returns, but also never below the 47th percentile. He was never a performance chasing manager, and was not in any particular year celebrated as a top-performer. But zooming out, guess where his returns ranked over the whole 14-year period?

That’s right, in the 4th percentile!

Conversely, managers found in the 5th percentile in any year, were also likely it be found below the 95th percentile (the bottom 5%) another year. The lesson of the story is that consistency matters over the long-term.

Reducing the Risk of Permanent Loss

Tying into the theme of avoiding the 95th percentile, the central objective of diversification is not return maximization, but risk management; specifically, reducing the risk of permanent loss.

Temporary declines are a normal part of investing. Permanent loss occurs when capital is impaired to the point where recovery becomes unlikely or requires disproportionate risk. Highly concentrated portfolios (such as stock-only, or, even worse, crypto-only strategies) are more vulnerable to such outcomes because they rely heavily on a narrow set of assumptions being correct.

Diversification spreads exposure across multiple drivers of return. This reduces dependence on any single economic scenario and increases the likelihood that the portfolio remains viable even when conditions are adverse.

Supporting Discipline and Rebalancing

Diversification also plays a critical behavioral role. By smoothing outcomes and reducing extreme volatility, it helps investors remain invested during periods of stress. This, in turn, supports disciplined behavior such as rebalancing, systematically adjusting allocations to maintain balance over time.

We become less prone to giving up and walking away from the markets at the bottom, only to miss a mighty recovery (cementing a permanent loss). If the portfolio drawdown is more shallow, thanks to diversifiers, we might avoid scars that are hard to wash off.

Rebalancing is only possible when a portfolio contains assets that behave differently. It is through this process that diversification can potentially contribute to long-term compounding, not by predicting winners, but by repeatedly restoring balance.

Volatility vs. True Risk

A final misconception is the conflation of volatility with risk. Volatility is observable and immediate; true risk is often structural and slow-moving.

An asset can be volatile yet resilient, or stable yet fragile. Gold is an excellent example of this (high volatility asset with portfolio balancing characteristics). Diversification seeks to manage true risk by limiting exposure to outcomes that could irreversibly damage the portfolio. In doing so, it may accept short-term volatility as a lesser concern.

Understanding this distinction is key to appreciating why diversification can feel uncomfortable even when it is functioning as intended.

HOW ALL-WEATHER / ALL-SEASONS PORTFOLIOS USE DIVERSIFICATION

All-Weather or All-Seasons Portfolio frameworks take diversification one step further by explicitly recognising that different assets perform well in different economic environments.

Rather than relying on forecasts, these approaches focus on structural exposure to a range of conditions that have historically occurred, and are likely to occur again.

Broadly speaking, economic environments can be described along two dimensions: growth and inflation. Growth can accelerate or decelerate; inflation can rise or fall. The combination of these forces creates distinct regimes, each favoring different types of assets.

Growth-oriented environments tend to support risk-seeking assets. Disinflationary or recessionary environments often favor defensive or interest-rate sensitive assets. Inflationary environments can reward real assets or inflation-linked exposures. No single asset performs well across all regimes.

An All-Seasons Portfolio accepts this reality. Instead of attempting to time regime shifts, it maintains diversified exposure across assets that respond differently to changes in growth and inflation. The portfolio is designed to be resilient rather than optimized for any single scenario.

This is also where it goes way beyond a traditional 60/40 Portfolio with arbitrary balance and lacking inflation-protection. You can read more on this topic in a separate article explaining why the 60/40 Portfolio is not balanced.

Patience and consistency are integral to this approach. The benefits of diversification emerge over time, through cycles that may test conviction. Short-term underperformance in one component is not a signal to abandon the framework, but an expected feature of maintaining balance.

By design, such portfolios rarely look “perfect” in hindsight for any single period. Their objective is not to win every year, but to remain robust across many.

THE ALL-SEASONS PORTFOLIO AND DIVERSIFICATION

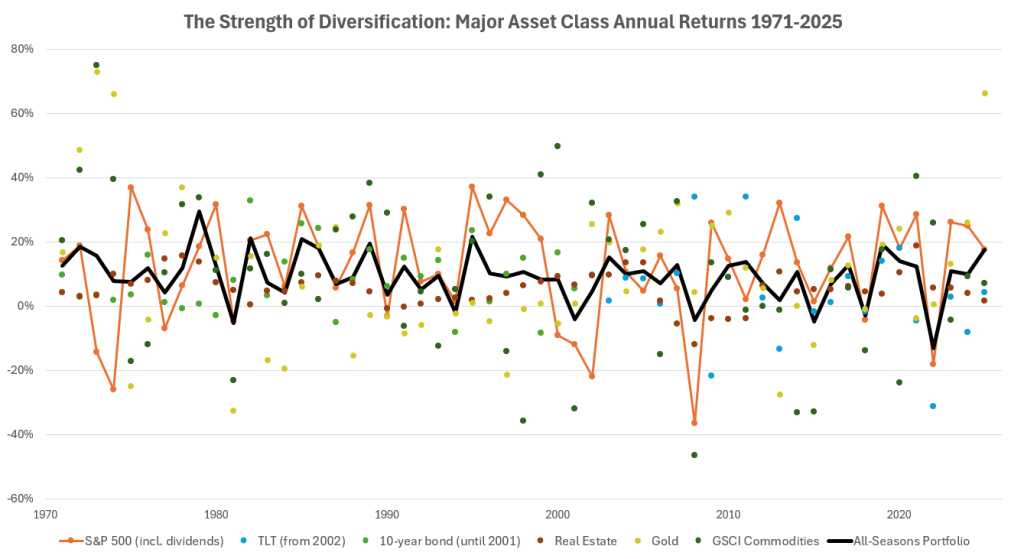

Let’s return to the chart at the beginning of this article. Only, this time, we add another line, which includes a simple All-Seasons Portfolio (the black line). The allocation for this portfolio is 30% stocks, 35% government bonds, 10% real estate, 15% gold, and 10% commodities, with annual rebalancing. This model portfolio is close to the one I manage as a Popular Investor on eToro.

Comparing to stocks, the most visible theme is that the line is much more centered along its mean. Additionally, in 17 years of the 55-year period, the All-Seasons Portfolio outperformed the S&P 500 (31% of the time), despite only having 30% stock allocation. Not bad for a “boring” and defensive strategy.

Only 7 times was the returns negative (11 for stocks); mostly only just below 0% return, with the worst drawdown being -13% (-36% for stocks).

The All-Seasons Portfolio has managed an arithmetic average annual return of 9.4% over the period, which is in the upper part of the interval of expected stock market returns (7-10%).

As for standard deviation – a measure of volatility – it comes in at just 7.8% for the All-Seasons Portfolio over this period, which is substantially lower than the 16.9% figure for the S&P 500.

Logically, diversification thus makes a lot of sense. Over time, you achieve the same levels of returns, but with a lot less variability. But when you are living through it on a year-by-year basis, and the stock market yields 25% when your diversified portfolio is “only” up 12%, it is psychologically difficult to maintain the chosen path.

This is when you need to remind yourself of why you diversify. You avoid the deep drawdowns, which are impossible to anticipate in advance. Conviction and logic remain your best friends during such times, and you will thank yourself when the stock market returns -25%. You just need to remind you of that when psychology tells you otherwise in the short-term.

WHY DIVERSIFICATION REQUIRES COMMITMENT, NOT OPTIMISM

Diversification does not require optimism about markets or specific assets. It requires commitment to a process – a set of rules you place for yourself based on logic and soundness.

The most common way diversification fails is not through poor design, but through abandonment. When one component underperforms for an extended period, the temptation to remove it can become overwhelming. Yet doing so often undermines the very protection diversification was meant to provide.

Gold was bad in the 1990s but has excelled ever since. Commodities were a drag 2005-2015 and in 2020, but has been great in the 1970s, 1980s and 2020s. Stocks delivered a lost-decade in the 2000s and were underperforming in the 1970s, but outperformed in the 2010s.

Abandoning diversification during periods of doubt typically means increasing exposure to what has already worked. This can improve short-term comfort but often increases long-term vulnerability.

Diversification works not because it avoids discomfort, but because it accepts it. The presence of uncertainty, disagreement, and uneven performance is not a sign of failure; it is evidence that the portfolio is not overly dependent on a single outcome.

In this sense, discomfort is the price of robustness. The alternative – concentration – may feel better when conditions align, but it carries a higher cost when they do not.

Sticking with diversification requires a clear understanding of its purpose and limitations. It requires evaluating success over full cycles rather than short intervals. And it requires resisting the urge to constantly revise strategy based on recent outcomes.

Final words

Diversification feels wrong precisely because it protects against futures we cannot confidently imagine. It asks investors to hold assets they may not currently like, understand, or believe in, in exchange for resilience across uncertain conditions.

This discomfort is not a sign that diversification is failing. It is often a sign that it is doing its job.

By reducing dependence on any single forecast, asset, or narrative, diversification shifts the focus from prediction to preparation. It prioritizes survival, discipline, and long-term compounding over short-term gratification.

In a world defined by uncertainty, this trade-off is not always emotionally satisfying, but it is structurally sound.

This philosophy underpins real-world All-Weather Portfolio frameworks that emphasize balance, patience, and robustness over market cycles: quietly, consistently, and without the need for constant conviction in any single outcome. It does not shine in any single year as the most fantastic strategy, but – more importantly – it is never found deep under water.

If you want to discover more about All-Seasons style investing, you can explore other topics on this website, or follow me on eToro – a highly recognised social trading platform – where I have been managing and shared content about All-Weather investing since early 2020. There, you can also automatically copy my portfolio and trade via eToro’s handy CopyTrading function, without extra costs or hassle. You find my profile by searching for @AllSeasonsPort, and you can also find an independently produced fact sheet at BullAware.com (updated monthly).

Data Sources

All annual asset return data besides TLT and GSCI: https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

TLT: https://totalrealreturns.com/n/TLT

GSCI: https://www.investing.com/indices/sp-gsci-commodity-total-return-historical-data

Photo by engin akyurt on Unsplash

{kind=link}

Great article, a few points to consider:

“As it is a feature rather than a bug, we can also take advantage of it when we rebalance the portfolio. This is exactly when the rebalancing premium is earned: when selling relative winners to buy relative losers, and over time earn more money than the average return of the owned assets.”

There is a downside to this, that it is not rare when after selling the winners they still keep growing, and the losers keep falling, in 2026 this is still visible with stock funds versus long-term bond funds and obviously we have no certainty that this would not continue further for many years ahead especially if the overall environment remains strongly inflationaty, damaging bonds, the longer the worse the damage is.

The incorporate this point (and the others) I divided my own portfolio into this rebalancing/dollar cost averaging portion and the no-touch/buy and hold/don’t sell, rebalance by buying more portion. I feel this is also part of the all-weather thinking, but not in terms of asset class selection, but investing strategy diversification.

In my own version of the all-weather portfolio I also maintain a bloc devoted to regional diversification, however imperfect, which includes a part devoted to the region I currently reside, in my case – Europe. This is due to the recent developments regarding sovereignty of all kinds, and the world seemingly going into a regional divide to an yet u known degree.

Thanks a lot Nikolai!

I agree with your point, but wanted to keep it light and simple in this article with a more general scope.

There are plenty of opportunities to be smart with rebalancing, and I have in the past written an article about Strategic Rebalancing which explores this concept. For example, in my eToro portfolio, I mainly rely on trend signals combined with partial rebalancings to ensure there is not too much drift from aimed allocations.

I think that this exactly captures your concern of selling winners too early.

It sounds wise too to diversify geographically, both in terms of exposures (EU underlying assets) and products (EU listed ETFs). This is something I have in mind too, deriving it from the book “The Permanent Portfolio: Harry Browne’s Long-Term Investment Strategy“, which discusses this to some extent.

Awesome remaks, Nicholas! Thank you! As a question not directly related to this, did you get or do you get any value from this – “Since 2025, I hold an International Certificate in Investment and Wealth Management (Level 3) from the Chartered Institute for Securities and Investment (CISI)”?