In this post, we will be discussing:

- Why you should be tracking the volatility and the trends of such volatility for the assets in your portfolio

- Why an Inverse Volatility Portfolio Optimizer can be a useful tool for a retail investor using risk parity strategies

- About the Volatility Analyzer tool that I have built in Google Sheets and the Inverse Volatility Portfolio Optimizer built into it

- How I use the tool for my investments in an All Seasons Portfolio environment when trading on eToro

- Book tip: Adaptive Asset Allocation by the principals of Resolve Asset Management, who manage several funds with dynamic risk parity strategies (link at the bottom of this post)

As an investor who has adopted a risk parity mindset, and perhaps have implemented a portfolio following risk parity principles, such as the All Seasons Portfolio, I am sure you at least have a fundamental understanding of the importance of volatility.

In several articles, I have discussed why it is vital for retail investors in particular to decrease portfolio volatility, and using another term, to decrease portfolio risk. Otherwise, we risk not achieving our financial goals, if we would encounter bigger drawdowns than we can afford, or that we allocate too much capital to a single asset class such as stocks when such assets face a period of lagging returns.

So, if the question is “How can I reduce portfolio volatility”, the answer is Risk Parity. Using these types of strategies and investing in several asset classes and allocating capital based on the asset classes’ relative risk, you can significantly decrease the overall volatility of your portfolio, while still earning the risk premiums of each asset.

But when it comes to risk parity, there are several ways it can be implemented.

Firstly, you have to decide on your overall portfolio strategy: do you want to balance the risk between your assets on a dynamic or static basis? Rephrasing this question, it relates to whether or not you are willing to continuously change the allocation between your assets as the volatility changes. For example, the All Seasons Portfolio is a static portfolio, as the risk balance is allocated based on the assets’ long-term mean volatility. Hence, a 30% allocation to stocks will continue to be 30%.

A dynamic approach, on the other hand, means that you will have a shorter lookback period for the attribute you are basing your balance on, for example volatility or covariance. As these tend to change over time, you must dynamically change your assets’ relative weights when their relative volatility changes. Depending on how short lookback period you have, the more often you will have to rebalance.

The second question to ask is what measure of “risk” are you balancing? As just alluded to, two examples of measure to base your portfolio weights on are volatility and covariance. At the end of the day, managing risk is about drawdown control, which is what you achieve through proper risk parity investing.

To facilitate management of risk, I have developed a Volatility Analyzer tool that also includes an Inverse Volatility Portfolio Optimizer. I first and foremost developed this for my own needs, which I will describe further below, but have found that it may be a useful resource also for you.

Why should you track volatility?

In investing, few things are possible to accurately predict. Predicting future return has been the Holy Grail of investing, but it is simply not possible to any significant degree of certainty predict changes in returns even on short horizons.

Even though Markowitz in 1952 introduced modern portfolio theory, with which he created a model for optimal portfolio allocation for maximizing the return per unit of risk, the issue with this, and any further development throughout the decades, is that the optimizers are based on historical returns – a measure famously not fit for prediction of future returns.

What investors have been more successful in predicting is actually volatility and correlation. Simply put, while if the market goes up today, it serves as no indicator for whether the market will continue rising tomorrow, an increase in volatility today has actually been a good predictor of that volatility will be elevated also tomorrow.

This was proven by Robert Engle and for his research, he was awarded the Noble Prize in 2003 on his work on new statistical models of volatility that captured the tendency of stock prices and other financial variables to move between high volatility and low volatility periods (“Autoregressive Conditional Heteroskedasticity: ARCH”).

Furthermore, it has been proven that a relative increase in volatility not only coincides with negative return, but typically also coincides with an increase in correlation between different assets (Haas, Mittnik, 2009). Volatility is persistent when it occurs, sometimes described as clustering, as high volatility in the recent past tends to be followed by high volatility in the recent future.

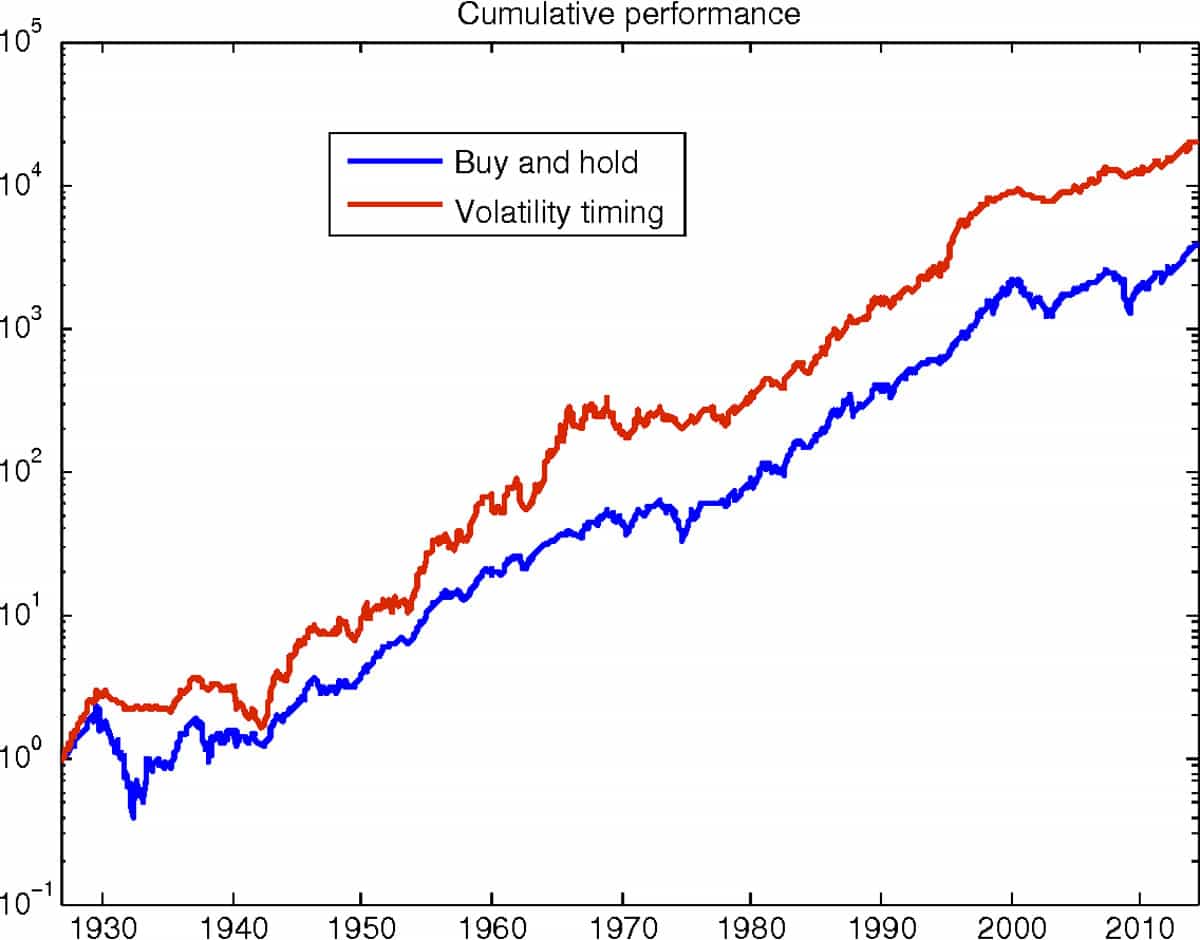

By anticipating volatility and correlation, it is possible to improve the risk adjusted return (Moreira, Muir, 2016). This means that strategies focusing on predicting risk, will decrease allocation to stocks during periods of expected high risk and increasing the allocation to stocks during a period of expected low risk. Such strategies usually outperform a classical buy-and-hold strategy.

Thus, it is a widely accepted Returns and Volatility of an asset are negatively correlated, and that you can improve your risk-adjusted return through predicting risk.

This becomes especially true during so called bad news events, during which volatility often increases and returns sharply decline, causing negative correlation.

Take the March 2021 Covid-19 crash for example. The low-point of Rolling 1M return of the S&P 500 was -30% by March 23, as the index had dropped form 3225.89 on February 24 to 2237.40 on March 23. At the same date, the rolling 1M volatility measured in annualized standard deviation (another term for volatility) had jumped to 0.80 from 0.17 a month prior. This clearly shows the negative correlation of these two measures.

While retail investors rarely have ARCH models available (and I am yet to be able to produce one to fit in a Google Sheets file), you will have to find alternative ways to analyze the volatility of your portfolio to make better informed investments.

Why you should use an Inverse Volatility Portfolio Optimizer?

If you are after a dynamic approach to risk parity to improve your odds for increased risk-adjusted return, it is wise to begin tracking the volatility of the assets in your portfolio.

One way of investing using this information is by implementing an Inverse Volatility rule to your asset allocation.

This means that your allocation to different assets will be based on an inverse relationship of their relative volatility. Hence, less capital will be allocated to an asset with higher volatility and vice versa.

With a shorter lookback period for measuring volatility, such as rolling 1-month periods, you will be better equipped to track and adapt your portfolio with little lag to the prevailing market environment.

Due to the negative correlation between returns and volatility, and Inverse Volatility strategy can be seen as a trend-following strategy and a short straddle, as your sell assets expected to experience negative return (after a relative increasing in volatility) and by assets expected to experience positive return (after a relative decrease in volatility). This is similar to a dynamic long straddle in the area of options trading where you buy put and call OTM contracts around a certain strike price, when yiu bet on increased volatility (you make money when the price of the underlying asset moves outside your straddle). For a trend-following strategy, scaling holdings works the same way as you sell on falling prices (increase in volatility) and buy on increasing prices (decrease in volatility).

Note also that Inverse Volatility strategies work best with assets with similar expected Sharpe ratios, as discussed in a whitepaper on portfolio optimization by Resolve Asset Management.

Note however, that Inverse Volatility portfolios do not take into account each asset’s biases to changes in expected economic growth or inflation. You thus need to be careful in your implementation to keep your exposures to different market regimes under control.

While I share no investment advice, from my personal use so far of an Inverse Volatility Portfolio Optimizer and from the backtesting of my particular portfolio, I have found that shorter lookback periods of about 1 month (and with a higher weight attributed to past months closer to today) tend to provide the best results when being rather active with rebalancing the portfolio. However, I have only tested this in August so far for a very specific set of portfolios why results may vary over time. And with a less active approach to portfolio management, longer lookback periods may work just as well.

About my Volatility Analyzer tool including an Inverse Volatility Portfolio Optimizer

Based on all of the above, to easily implement an Inverse Volatility strategy, you need a tool that helps you analyze the volatility of your assets and to make the calculations for portfolio allocation, it helps to have a tool that does this for you.

As most retail investors, myself included, do not have access to expensive investing software, I built the Volatility Analyzer tool using the easiest data program I had at hand: Google Sheets.

While Excel is great, Google Sheets’ built-in functions that retrieve market data for thousands of international stocks and ETFs and which is not tied to an annual subscription, this became my resource of choice. I am sure you also have easy access to a Google account.

Examples of a couple of typical use cases of an Inverse Volatility Portfolio Optimizer include:

- Dynamic Risk Parity Portfolio management for certain types of risk parity strategies.

- Better understand volatility of portfolio components and the trends of such volatility.

- Improve performance through strategic rebalancing (timing of rebalancing events) determined by trends based on asset classes’ relative volatility.

- Bottom-up risk parity approach where Inverse Volatility is used within an asset class, for example stocks.

The sheet consists of two main components:

- A Volatility Analyzer that gives a good overview of the trends in volatility; and

- An Inverse Volatility Portfolio Optimizer.

The tool is built to support 15 assets and a lookback period of 12 months for volatility in relation to the portfolio optimizer.

Let’s have a quick look at both of these functions, using a few American ETFs as an example. The file supports both European and American listed ETFs. A deeper description of the functions is included in the PDF accompanying the purchased access.

Volatility Analyzer

The Volatility Analyzer part of the sheet provides an overview of the current volatility using several periods’ lookback (1M to 2Y), in addition to the trends and changes in Rolling 1M volatility.

You will also find tables and charts over past performance of Rolling 1M and Rolling 3M volatility for the last 2 years.

As discussed above on the negative correlation between returns and volatility, you will also find data over the correlation between rolling 1M return and rolling 1M volatility to better understand the assets’ performance and risk.

Inverse Volatility Portfolio Optimizer

The second part of the tool is the Inverse Volatility Portfolio Optimizer.

With this, you can easily build portfolios based on the assets’ relative inverse volatility.

The sheet includes backtesting functionality for the last 6M and with comparisons with an equal weight portfolio with the same assets, and benchmarks the S&P 500, a 60/40 portfolio and a global stock ETF.

The optimizer is built to accommodate assets denominated in both EUR and USD. Just update the “Your Domicile” cell to show a correct comparison against the benchmarks denominated in the same currency as your portfolio (for example, if your portfolio is mainly traded in EUR, it is more relevant to compare performance against a S&P 500 ETF also denominated in EUR).

You can manually select the lookback period for volatility (1M-12M) and set the weights for each month. To get started, you can opt to use the buttons “Equal Weight” and Front Loaded to set the weights.

All in all, I find this an easy to use tool for managing an Inverse Volatility Portfolio. You find it on the Investing Tools page, or by following the link below:

Did you know that from now, all who support the blog on Patreon always get 20% off on all items in the Investing Tools page, including this Inverse Volatility Portfolio Optimizer, regardless how long you have been supporting the blog.

You can sign up for a patronage as small as €1, and find the discount code in the pinned post. This means that by signing up, you would immediately get a net €3 discount on the Volatility Analyzer and Portfolio Optimizer.

Additionally, all support for sustaining this website – which is currently run on a hobby/side project basis – would be greatly appreciated!

How I use the Volatility Analyzer and Inverse Volatility Portfolio Optimizer

As alluded to earlier, I began building this volatility analysis tool for my own portfolio management purposes.

The basis of my portfolio is, and will remain, the All Seasons Portfolio strategy, meaning that I will keep having a static asset allocation based on the long-term mean volatility of stocks, bonds, inflation-linked bonds, gold, and commodities as a base.

I currently run the All Seasons Portfolio on two different platforms.

Firstly, I run it on Degiro using UCITS ETFs. This is the portfolio I have been describing in detail on this blog for the past two and a half years.

Secondly, I run it on eToro since 1 April 2021. Here I decided to do it with a bit more advanced approach. For example, this portfolio is levered around 1.30x-1.35x as I use a 3x levered long-term government bonds ETF.

To further improve my risk-adjusted return on this eToro portfolio, I have decided that in addition to a top-down approach to risk parity (meaning risk parity between asset classes), I wanted to included also a bottom-up risk parity approach, which means that I apply risk parity also within asset classes.

Based on what I discussed above that the Inverse Volatility strategy works best for assets with similar expected Sharpe ratios, I found this to be a great strategy to implement for one of the asset classes in a bottom-up risk parity environment.

Thus, for the stock part of the portfolio, which is 40% now that the total portfolio is levered around 1.35x, I have implemented the Inverse Volatility strategy.

The stocks ETFs I use is a selection of ETFs which in aggregate provide a global exposure. For example, they provide exposure to the S&P 500, Nasdaq, Dow Jones, Russell 2000, Europe, Emerging Markets, and Japan.

For achieving improved risk-adjusted return based on the theory described in this article, I will be allocating my capital to each of these ETFs based on Inverse Volatility. As they all belong to the same asset class – stocks – the expected Sharpe ratio for these ETFs are similar, why Inverse Volatility is an appropriate strategy to implement (see reference to Resolve Asset Management’s whitepaper).

As I am (relatively) active on eToro, overseeing my portfolio daily, I have elected to have a short lookback period of 1 month for determining the trends in volatility. I will thus rebalance the stock ETFs about every other week as their relative volatility change.

Check out my portfolio on eToro by searching for user “Allseasonsport”.

Book tip: Adaptive Asset Allocation by Adam Butler, Michael Philbrick and Rodrigo Gordillo

Above, I already linked to one article written by Adam Butler a Resolve Asset Management – a well-renowned fund manager on the risk parity scene – being the whitepaper on portfolio optmimization.

The team is doing a great job in marketing and educating Risk Parity as a strategy for both institutional and retail investors. They are active in publishing new articles and papers, as well as running a great podcast on exciting topics around risk parity investing. I highly recommend both types of content from Resolve, which can be found for free on their website investresolve.com.

But another great piece of work from the team is the book that they published called Adaptive Asset Allocation. This is more aimed toward retail investors and is highlighting how you can implement strategies that are adaptive to changes in market environments for better risk management in your portfolio. Inverse Volatility is one such strategy that can help you decrease drawdowns.

By reading Adaptive Asset Allocation, you will learn how to build an agile, responsive portfolio with a new approach to global asset allocation

Adaptive Asset Allocation is a no-nonsense how-to guide for dynamic portfolio management. This book walks you through a uniquely objective and unbiased investment philosophy and provides clear guidelines for execution. From foundational concepts and timing to forecasting and portfolio optimization, this book shares insightful perspective on portfolio adaptation that can improve any investment strategy. Accessible explanations of both classical and contemporary research support the methodologies presented, bolstered by the authors’ own capstone case study showing the direct impact of this approach on the individual investor.

Financial advisors are competing in an increasingly commoditized environment, with the added burden of two substantial bear markets in the last 15 years. This book presents a framework that addresses the major challenges both advisors and investors face, emphasizing the importance of an agile, globally-diversified portfolio.

- Drill down to the most important concepts in wealth management

- Optimize portfolio performance with careful timing of savings and withdrawals

- Forecast returns 80% more accurately than assuming long-term averages

- Adopt an investment framework for stability, growth, and maximum income

An optimized portfolio must be structured in a way that allows quick response to changes in asset class risks and relationships, and the flexibility to continually adapt to market changes. To execute such an ambitious strategy, it is essential to have a strong grasp of foundational wealth management concepts, a reliable system of forecasting, and a clear understanding of the merits of individual investment methods. Adaptive Asset Allocation provides critical background information alongside a streamlined framework for improving portfolio performance.

For more reading on risk parity investing, check out my earlier article on 3 great books on Risk Parity for learning more about these types of strategies that aim to lower your portfolio risk and thus improving your risk-adjusted returns.

{kind=link}