Volatility Analyzer Tool and Inverse Volatility Portfolio Optimizer (Google Sheets)

€ 10

The Volatility Analyzer spreadsheet is a useful tool to better understand the trend in volatility of the assets in your chosen portfolio.

The sheet also includes a Portfolio Optimizer built on Inverse Volatility principles, meaning that it constructs an optimal portfolio which weighs the assets inversely based on their relative volatility. Hence, an asset with higher volatility receives a lower allocation of funds invested, and vice versa.

The spreadsheet is built to support portfolios of up to 15 assets and with 12-month lookback period for the volatility analysis of the portfolio optimizer.

Upon purchase, you will receive a PDF containing a link to the Google Sheets file, and instructions for making a copy to yourself, as well as further information and instructions of how to use the sheets.

As I have limited monetization of this blog, I kindly request that you don’t share the sheet further other than by sharing the link to this shop site. Thank you.

Don’t forget that all Patreon’s, regardless of how long you have been a Patreon, always receive 20% discount on all products in the shop. Become a Patreon for a little as €1 per month to support my work on maintaining this site.

Description

Volatility is negatively correlated with returns.

It is thus vital for any investor to better understand the volatility and the trend of volatility of each asset in one’s portfolio. When volatility spikes for risk assets, it most commonly coincides with a sharp decline in returns in the short term.

From this knowledge, a popular dynamic risk parity portfolio strategy has been developed, being the Inverse Volatility strategy. This means that you construct a portfolio where capital is allocated to each asset based on their inverse relative volatility – more capital is allocated to a low-volatility asset, and less capital is allocated to a high-volatility asset. As volatility is ever-changing, it is common practice to actively rebalance the portfolio based on the changes in rolling volatility.

The Volatility Analyzer Tool and Inverse Volatility Portfolio Optimizer, powered by Google Sheets, therefore includes two main components:

- A Volatility Analyzer providing you with an overview of the trends in volatility of a portfolio of up to 15 assets; and

- An Inverse Volatility Portfolio Optimizer where you can adjust the lookback period for volatility (1 month to 12 months) and attribute how much weight each of the months shall have in the analysis.

Volatility Analyzer

The Volatility Analyzer part of the sheet provides an overview of the current volatility using several periods’ lookback (1M to 2Y), in addition to the trends and changes in Rolling 1M volatility.

You will also find tables and charts over past performance of Rolling 1M and Rolling 3M volatility for the last 2 years.

You will also find data over the correlation between rolling 1M return and rolling 1M volatility to better understand the assets’ performance and risk.

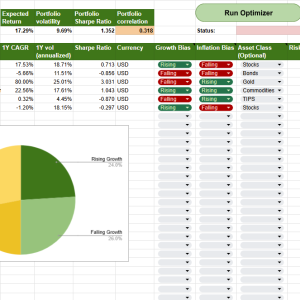

Inverse Volatility Portfolio Optimizer

The second part of the tool is the Inverse Volatility Portfolio Optimizer.

With this, you can easily build portfolios based on the assets’ relative inverse volatility. The sheet includes backtesting functionality for the last 6M and with comparisons with an equal weight portfolio with the same assets, and benchmarks the S&P 500, a 60/40 portfolio and a global stock ETF.

The optimizer is built to accommodate assets denominated in both EUR and USD. Just update the “Your Domicile” cell to show a correct comparison against the benchmarks denominated in the same currency as your portfolio (for example, if your portfolio is mainly traded in EUR, it is more relevant to compare performance against a S&P 500 ETF also denominated in EUR).

You can manually select the lookback period for volatility (1M-12M) and set the weights for each month. To get started, you can opt to use the buttons “Equal Weight” and Front Loaded to set the weights.

How I use the Portfolio Optimizer

In my All Seasons Portfolio that I run on eToro, I have applied this Inverse Volatility Portfolio Optimizer for the stocks part of the portfolio. I thus have 7 different ETFs with different sector/geographical exposure (S&P 500, Nasdaq, Dow Jones, Russell 2000, Europe, Emerging Markets, Japan, etc.) and allocate the capital per inverse volatility to further improve the risk-adjusted returns of my portfolio. As I am rather actively overseeing that period, I use 1M lookback for volatility. Consider following me on eToro to see how I perform, and if you like what you see, you can also opt to copy my portfolio starting with a small amount.

Reviews

There are no reviews yet.