Hi, and good to have you back for another article related to risk balanced portfolio investing!

If there is anything investors have learned (or at least should have learned – memory is short) during the 2020s, it is that central bank interest rates carry a lot of external risk for any investment portfolio.

We have seen inflation spike in 2022, with a sharp rise in interest rates to combat it. This has caused a broad range of risk assets to plunge, and the pain was felt by many retail investors and retirees.

Interest rate risk is an important type of risk to be aware of as an investor, as it affects stocks and bonds indiscriminately. That is especially harmful for investors only investing in stocks or using a “balanced” stock-bond portfolio.

We will therefore be taking a closer look at what it is and whether there is anything we can do as investors to protect our wealth and portfolios against it. But let’s begin with a bit of background to what transpired.

Interest rates in the 2010s

As a response to the negative economic effects of the Covid-19 pandemic, central banks across the globe swiftly and severely decreased steering and repo rates – often to levels close to or even below zero.

Coupled with central bank asset purchases, the aim was to ensure functioning and liquid capital markets and facilitating for as many companies as possible to survive the worst phases of the pandemic.

The overall trend in interest rates have, however, been in a steady decline for four decades already, with key European rates reaching negative territory in the 2010s (ECB in 2014, Bank of Japan in 2016 and Denmark’s Nationalbank in 2012, to name a few).

The Fed has not (yet?) had to turn to negative rates, but is the clearest proxy of the prevailing interest rate trend, as the steering rate topped out at around 20% in March 1980, and bottoming out (again) at 0.25% in 2020. The rate was at the same levels after the 2008 financial crisis, before a temporary increase in 2018 to 2.5%.

Central bank steering rates are not isolated in any way, but these do to a vast extent impact the capital markets. Government Bond yields at different parts of the yield curve are “set” by the market participants as forecasts on where the short term bond yields will be at any time in the future.

For many years, investors and economists have continued to claim that “interest rates and yields can’t fall any lower than they are today”, but every time, that is exactly what has happened. That has meant that the German 10Y bund has also been trading in deeply negative territory, and the American treasury bond with the equivalent tenor traded at a low yield of 0.566 in September 2020.

While the Fed, the ECB, and other central banks control the short-term interest rate, longer-term yields are merely reflections of the market’s future expectations of short-term rates.

As the market is expecting higher rates in the future, which will impact the financing costs of companies and consumers, this is manifested in the yields of bonds with different maturities. Hence, as central banks have been increasingly vocal about hiking rates, in addition to tapering asset purchase programs, this is being reflected in the bond market already now. This also leaks into other assets, such as stocks as well. Hence, rising rates is an investment risk that is hard protect against.

What is interest rate risk?

But let’s take a few steps back and first more carefully answering the question what is interest rate risk?

Interest rate risk is a type of risk that is hard to directly diversify away, as it impacts both fixed-income assets and stocks, albeit in slightly different way.

Bonds are more directly impacted by this risk type, as when rates rise, the price of bonds decline due to opportunity cost of holding a bond.

For example, if a bond is paying you 1.5% per year, and the rate rises to 2%, then it would be more beneficial for the bond investor to sell the first lower-yielding bond and buying a freshly issued one with higher yield that matches the increased rate.

As the market is quite effective, the price of the first bond will fall, so that the effective yield of the bond matches what you would earn with the higher-yielding bond. Hence, as rates rise, bonds will be falling in value.

Rising rates impact bonds with shorter tenors more than bonds with longer tenors. This can be explained by the certainty of expectations. It is easier to predict tomorrow’s weather, than whether the sun will be shining in three weeks’ time. The shorter the timeframe, the higher certainty that the expectations will be true.

This effect is exacerbated by the fact that most central bank communicate their intended rate paths, which is their forecast for the steering rate. However, as it is a forecast rather than a promise, there is still room for the market to decipher what actions the central banks will take even in the near future.

Such forecasts change, and that is what has happened in the beginning of 2022. As the inflation rate has remained elevated, the Fed and ECB have changed course and communicated an intention to raise rates both more and sooner than what the markets previously had expected. This has lead to bonds falling in price.

But longer-term bonds (with 20+ year maturities) have been less affected by the latest rate hiking forecasts, as it appears that the market still believe that further out in the future, rates will have to remain low. One can only make qualified guesses on why that is the case, but common explanations for such expectations include that growth will be harder to achieve with an aging population and decreased globalization, why central banks may not lift its foot from the gas pedal entirely. And with such a high debt-to-GDP ratio as we see among many developed nations today, any meaningful hikes may not be possible even in the intermediate-term without crippling the economy.

As for stocks, the effects of rising rates are more indirect in nature, but they are still considerable.

Firstly, rising rates impact to borrowing costs of companies, as their operations are usually financed by bank loans, bonds, commercial papers, or a combination of the three in addition to the shareholders’ equity. The direct effect is thus that if rates rise, so does the cost of borrowing.

These days, rising yields is particularly problematic for interest expenses, as the so called “Zombie companies” make up a record share of the S&P 500 index. These are companies who only afford to service their debt (amortizations and interest) with their income, but don’t generate any shareholder value. In other words, these are companies with an interest coverage ratio (EBITDA divided by financial expenses) below 1.00x for three years in a row.

It is especially cumbersome that these companies are so great in number despite rates being as low as they are today. If rates were to increase, these companies would encounter even bigger problems. In such case, rising interest expenses would soon grow above its EBITDA, seriously harming the firm’s possibilities to survive for any meaningful time.

Secondly, the price of stocks is a product of equity risk premium over the risk free rate, meaning that interest rates is a crucial component of the expected return of stocks.

As a reminder of the capital asset pricing model (CAPM), the formula for calculating the expected return of the broader stock market, is Expected Return = Risk-Free Rate + Equity Risk Premium. The equity risk premium is usually estimated to be around 4% for blue-chip stocks. The risk-free rate is what an investor could earn by just holding the safest assets available, i.e., government bonds issued by credit-worthy countries.

To translate this to the language of bonds, this expected stock return is the “yield”, and when it rises, the price of the stocks will decline. That is exactly what happens when the risk-free rate component of the model rises.

As a consequence, when the risk-free rate, i.e., the short-term yield, rises, so does the required return of stocks, which has a negative effect of stock prices.

Therefore, when central banks raise rates – or even already when the communicate that they will raise rates – that has a dampening effect on both stock and bond prices.

Can you diversify from interest rate risk?

Now that we have established what interest rate risk is and how it negatively affects the prices of assets, the logical next question is: how can we protect against it?

The disappointing truth is that there is not much that can be done to hedge against future rising rates.

Especially if you are a stock investor or a 60/40 stock/bond investor, rising rates will increase the volatility of your portfolio. Rising rates would significantly impact these in your portfolio, and you’d be in for a certain drawdown.

Looking in the rearview mirror, for the past 40 years, we have been in a falling rate environment ever since 1981, so all-in-all, rising rates have been a negligible issue, as it has always fallen back down after a hike.

But if we instead look ahead, as Fed’s Powell and ECB’s Lagarde are promising rising rates, the undiversified investor is right to worry.

But as holding excessive amount of cash may not be the best idea as the purchasing power is being eroded by inflation (one of the reasons why I am not a follower of Harry Browne’s Permanent Portfolio), we better be looking for protection in the reasons why the rates are rising.

When rates rise, that is one of the few times when the return of cash can be expected to be higher than that of stocks and long-term bonds, as short-term notes are not falling as hard as long-duration assets.

What investments benefit from rising interest rates?

So, let’s back up a bit again. As you know, one of the central banks’ main task is to control inflation (we’ll not review here how good they are at it though…) and their number 1 weapon is the steering rate. When inflation falls below that magic 2% threshold, the central bank lowers its steering rate to spur investment and getting inflation going again, and when inflation is running too hot, the rate is hiked.

That means that to set up your well-diversified portfolio to return in excess of the cash rate also in times when interest rates are rising, you better make sure your portfolio does well in environments that cause rate hikes, that is, in inflationary environments.

Inflation-hedges come in different forms depending on what kind of inflation we are facing (Cost-Push inflation, Demand-Pull inflation, or inflation caused by increased money supply; I will post a short article about this in the near future). A diversified inflation-hedge comes from a combination of commodities (protecting against cost-push inflation), gold (protecting against inflation caused by increased money supply), and inflation-linked bonds/TIPS (protection against demand-pull inflation).

It is hard to protect against the effects of the event of rising rate expectations (especially when we are not interested in trying to predict what goes on in the head of central bank committee members). By always having a broadly diversified portfolio like the All Seasons Portfolio, you will benefit from the environment immediately before cash rates rise, and thus will see more stable returns in your portfolio.

As I have seen this a lot lately, that you could invest in the financial sector, as banks benefit from rising rates, I just want to point out that this is not really true. I will not spend much on this particular question but will just mention that while banks might earn higher interest rates, their funding rates rise correspondingly. In addition, as zombie companies today make up for a record share of the stock market (more than 20%), if rates rise, many of these companies will be forced to file for bankruptcy, with the risk of banks having to write off significant receivables and face capital losses. That is hardly good for a bank’s bottom line.

Investments that benefit from periods just before rates start rising

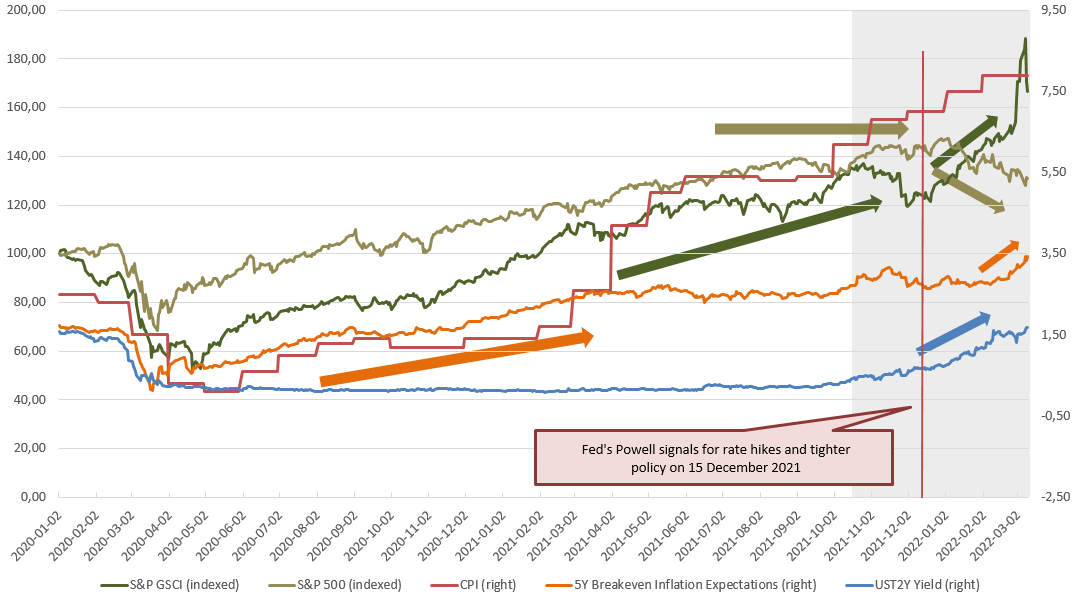

To illustrate how commodities have benefitted from the rising inflation expectations, I have summarized the performance since January 2020 in the chart below, and compared it with US YoY CPI prints (red line), 5Y Breakeven Inflation Expectations (UST5Y minus USTIP5Y; orange line), the UST2Y market yield (blue line) and the S&P 500 (gold line). During this period Fed’s funds rate has remained zero, so it has not been plotted.

While all of these measures fell in March 2020, both backward looking inflation and forward looking inflation expectations have been climbing steadily for the last two years. This is not at all surprising, driven by a combination of central bank stimulus, supply chain disruptions, and a change in consumer behaviour from buying services to buying more hard things on the back of Covid related restrictions.

This has pushed up commodity prices broadly (both energies and metals). The S&P 500 has seen a similar trend as well, albeit for other reasons, as central banks stimulating a recovery also of economic growth.

But if we zoom in a bit on the last four months, commodities and stocks have begun seeing different development. While stocks began stagnating already in September 2021, commodities kept moving upwards more sustainably. Especially after Fed’s Powell signaled for rate hikes and tighter monetary policy on the December 15 FOMC meeting (red vertical line), interest rate expectations (seen in the 2-year US Treasury Bond) began rising, and stocks began their decent. The UST2Y yield began creeping upwards already before that though (grey area of the chart).

Additionally, as you can read from the last increase of inflation expectations and rising commodity prices even before Russia’s illegal invasion of Ukraine, but that the latter really hockey-sticked.

It is likely, given the continuing rising measured inflation, that commodity prices would have continued to increase steadily even without a war on European soil, but that this has given the commodity prices a preemptive boost.

But all in all, the key take-away from this chart is that while interest rate risk harms some assets (see the stagnation of S&P 500 with the heightened expectation of rising rates), commodities is an asset class that has benefitted before the interest rate risk materialized, and has continued to perform well on the back of both rising measured inflation (CPI; a backward looking measure) and expected future inflation (5Y Breakeven rates).

The All Seasons Portfolio and rising rates

2022 to date shows the benefit of well-diversified and balanced risk parity portfolios. As these types of portfolios include uncorrelated assets that do well in different environments, there will always be at least one asset that gets to show its unique personality, regardless what happens in the world. Through the 2010s, that was stocks and long-term government bonds in a disinflationary environment. Now, it is commodities, gold, and inflation-linked bonds in an inflationary, and possibly slowing growth, environment.

While it is impossible to know with certainty in advance a) what inflation will be in the future and b) what central banks will do, it is important to always have a hedge in place in a portfolio.

The extraordinary events we have already witnessed in the last 2 years – a pandemic and a major war – it shows how vulnerable our world is and what underlying risks there are for economies. That of course has huge impact on financial assets.

As the past two years have been nothing like the “business as usual” times of the prior decade, a growing number of investors have fallen into a false sense of safety, and thereby neglecting due protection.

I am quite glad that I adopted a common-sense type of investing already in late 2019, as I learned about the All Seasons Portfolio strategy and risk parity strategies in general. I turned out to be unbelievably lucky with the timing.

The thing is, that well-diversified portfolios, with built-in protection against all major economic regimes that can be experience, is just common sense.

If you revisit the chart further up, you will see that stocks and commodities have identical returns from the beginning of 2020 until September 2021, but that commodities – an asset class that has been hated throughout the disinflationary 2010s – have since outperformed stocks.

Still, my All Seasons Portfolio has remained stable, and has actually kept growing in value through the war in Ukraine, as I will be showing here below.

If you are looking for getting started with your own All Seasons Portfolio and need some inspiration, check out my post on How to get started with the All Seasons Portfolio strategy. While stocks have been a great investment the last decade, there are no guarantees that this trend will last, as their continued success depends on several factors. Instead, consider diversifying your portfolio to include other asset classes, and benefit from the rebalancing period over the long-term, as described in this article.

Did you know that I have been a Popular Investor on eToro since 2020?

You can follow me there and copy my All Seasons Portfolio automatically, getting started with as little as $200. Just create an account and look up my profile (AllSeasonsPort).

If you want to see more portfolio data before you invest, just head over to the BullAware Fact Sheet for my portfolio, which is an independent data site for eToro profiles.

Thank you yet again for following my blog about risk parity investing and the All Seasons Portfolio. If you haven’t done so already, make sure to subscribe to the newsletter via the form in the page footer, and to drop any comments you may have on the content with the comment section or via email to nicholas@allseasonsportfolio.eu. The greatest value I have received from upkeeping this blog is the fantastic conversations with great people, such as yourselves, about ideas on investing and strategies. Thanks for that!

We’ll catch up soon,

Nicholas.

Want to show your support and help financing the maintenance of the blog through a one-time donation? Leave a sum of your choice, like $5, to the tip jar via Paypal (common credit cards supported). Any contributions are highly appreciated!

{kind=link}

Great article Nicholas. One naively thinks that with rising rates the best investment are short-term bonds and deposits. But if rates rise it is because inflation is rising, then the best investments become commodities, gold and inflation-linked bonds. Two different ways of approaching the problem. Henry Brown, for his permanent portfolio, proposes cash, Ray Dalio for his all-seasons suggests commodities, gold and TIPS and states that cash is junk!

Thank you so much Paolo!

I think both views are correct actually, but it depends on how you frame it.

Cash and short-term rates offer protection against interest rate risk when considering this in isolation (i.e. not from a portfolio perspective) and if you ONLY measure a period when interest rates rise (remember though that asset prices to a larger extent move on the market’s expectations of a hike, not on the de facto hike in rate that occurs afterwards).

But if you zoom out, holding cash and short-term rates offer little return in periods prior to or after an increase in rates. Also now, while cash would have offered protection for a rate hike, an inflation print of 7.9% in the US and 5.7% in Italy sets a big challenge for the cash position to actually provide you real returns even in a rate hike cycle. Still, when measured relative to stocks, then yes, cash is a better investment, but in a diversified portfolio with other assets as well, and when considering the period leading up to the rate increase, cash is unlikely to outperform such a portfolio.

While I covered rate hikes preceded by high inflation in this article, the only other reason to raise rates is when economic growth is rising fast, presumably after a prior recession that the central bank has wanted to stimulate a recovery from and rates are to be normalized. In relation to such rate hike, stocks would presumably have performed well in the period leading up to the increase in rates, and I think longer-term government bonds (20+ years) would presumably perform relatively better when the rate hike happens (as the rise in rates increases the probability for slowing growth and disinflation, which is good for safer assets). 10-year bonds I would expect should not do so well in that situation time either though.

So in terms of the two camps you describe, I’m in team “cash is trash”! 🙂

This was perhaps a somewhat half-baked answer, but hope it makes sense.